International

Japan Real Wages Rise for First Time in 13 Months

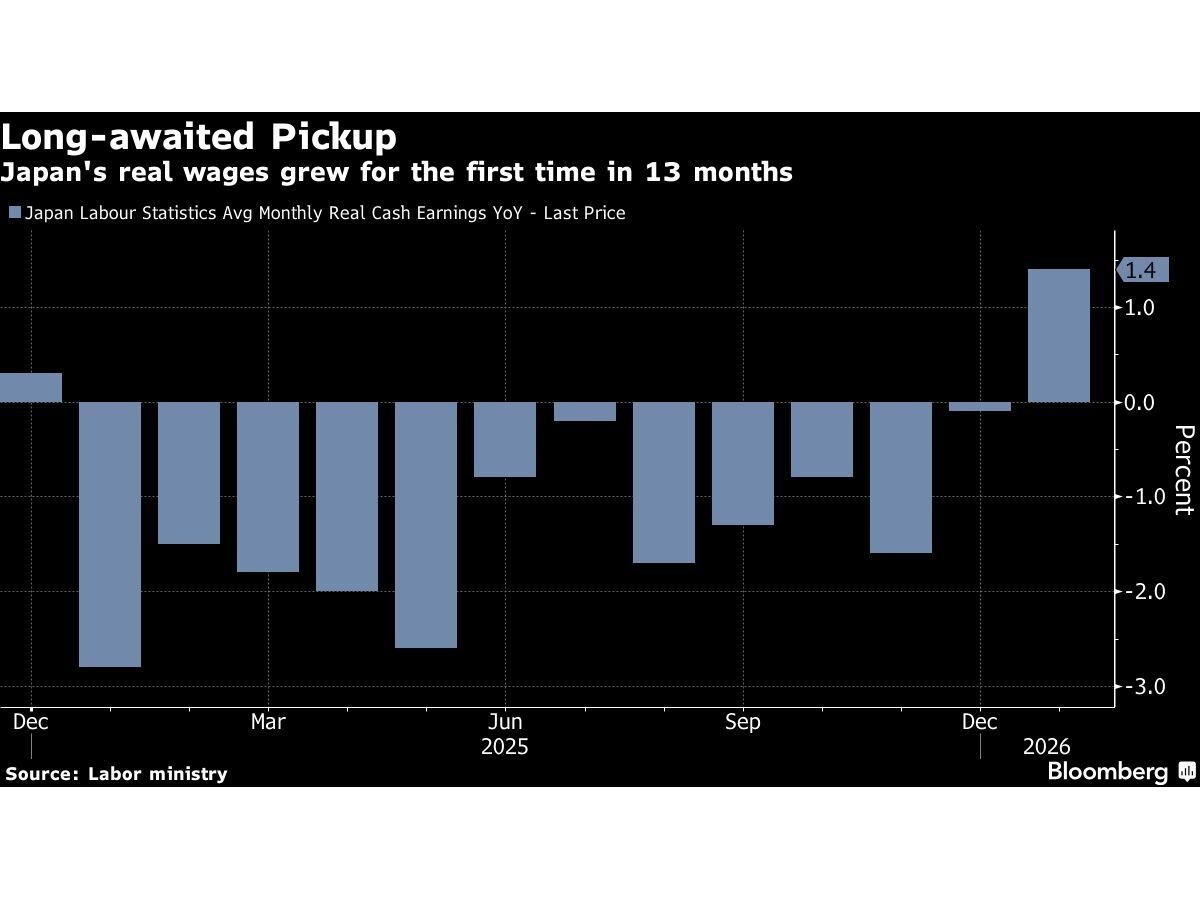

Japan’s real wages have increased for the first time in 13 months, a development that could strengthen the case for the Bank of Japan to continue raising interest rates as the country attempts to normalize its monetary policy.

Data released by Japan’s labour ministry showed that inflation-adjusted wages rose by 1.4 percent year-on-year in January, marking the first positive growth after more than a year of declines. Nominal wages also climbed by around 3 percent, reaching an average of about 301,000 yen ($1,900).

The increase in pay came as consumer inflation eased to roughly 1.7 percent, allowing wage growth to outpace price rises for the first time in months. Analysts say the development could boost household spending and provide support for Japan’s economic recovery.

Base salaries recorded their strongest growth since 1992, while overtime pay and bonus payments also increased, indicating improving labour market conditions across several sectors.

Economists say the stronger wage data could encourage the Bank of Japan to proceed with further interest-rate hikes after decades of ultra-loose monetary policy aimed at combating deflation. The central bank had already raised its benchmark rate to 0.75 percent in December 2025, the highest level in about 30 years.

The wage gains also come ahead of annual wage negotiations between Japanese companies and labour unions, with the country’s largest union federation pushing for nearly 6 percent pay increases in 2026 to sustain income growth.

However, economists caution that global factors, including rising energy prices linked to geopolitical tensions in the Middle East, could still affect Japan’s economic outlook and influence the timing of further rate hikes.

If wage growth continues and consumer spending strengthens, analysts say the central bank may feel more confident about tightening policy further as it gradually moves away from decades of aggressive stimulus.

The government of Burkina Faso has adopted a new National Development Plan (PND) for 2026–2030, a five-year economic roadmap estimated at about $64 billion, aimed at transforming the country’s economy, strengthening stability, and promoting inclusive growth.

Officials said the ambitious development framework is designed to guide national investment priorities over the next five years, focusing on rebuilding key sectors of the economy, improving infrastructure, and creating jobs.

According to government sources, the plan will prioritize investments in agriculture, energy, infrastructure, industrial development, and social services, with the aim of boosting productivity and improving living standards across the country.

Authorities noted that the program is also intended to address economic vulnerabilities while supporting national security and stability, as the West African nation continues to confront security challenges that have affected economic activity in recent years.

The government said both public and private sector investments will play a key role in financing the plan, with support expected from international development partners and regional institutions.

Economic analysts say the success of the initiative will depend largely on effective implementation, improved governance, and the country’s ability to attract foreign investment despite ongoing security concerns.

The new strategy replaces the country’s previous development framework and is expected to guide policy decisions, investment planning, and reforms through 2030 as Burkina Faso seeks to strengthen economic resilience and accelerate growth.

Officials say the plan reflects the government’s commitment to sustainable development and long-term economic transformation.

Iran has named Mojtaba Khamenei as the country’s new Supreme Leader following the death of his father, Ali Khamenei, marking the first time a son has succeeded his father in the position since the establishment of the Islamic Republic.

The appointment was made by Iran’s powerful Assembly of Experts, an 88-member clerical body responsible for selecting the country’s supreme leader. The council reportedly reached the decision after an extraordinary session convened in early March.

Mojtaba Khamenei, a 56-year-old cleric who has long operated behind the scenes in Iranian politics, is widely believed to have strong ties to the Islamic Revolutionary Guard Corps (IRGC). Analysts say his appointment reflects the growing influence of hardline factions within Iran’s security establishment.

His rise comes during a period of intense regional tensions following the reported killing of Ali Khamenei during strikes linked to the ongoing Middle East conflict. The situation has triggered military confrontations across the region and pushed global oil prices sharply higher amid fears of disruption to energy supplies.

Mojtaba Khamenei now becomes only the third supreme leader since Iran’s 1979 Islamic Revolution, placing him at the helm of the country’s political, religious, and military authority.

However, the succession has generated controversy both inside and outside Iran, with critics warning that the move could signal the emergence of a dynastic leadership system in a country founded on opposition to hereditary rule.

International reactions have been swift. The U.S. President Donald Trump criticized the appointment and warned that Iran’s new leadership would face significant pressure from Washington and its allies as tensions in the region continue to escalate.

Global oil prices have climbed above $115 per barrel for the first time in more than three and a half years as the ongoing conflict involving Iran, Israel and the United States continues to disrupt energy production and shipping across the Middle East.

Data from the Chicago Mercantile Exchange showed that the price of Brent crude, the international benchmark for oil, rose to $107.97 per barrel, marking a 16.5 percent increase from Friday’s closing price of $92.69.

Similarly, West Texas Intermediate (WTI), the main benchmark for U.S. crude oil, climbed to about $106.22 per barrel, representing a 16.9 percent rise from its previous close of $90.90.

The surge follows a sharp increase last week, when U.S. crude prices jumped 36 percent while Brent crude gained 28 percent, driven largely by fears of supply disruptions as the conflict entered its second week.

Strait of Hormuz Disruptions

A key factor in the price spike is the disruption of shipping through the strategically important Strait of Hormuz. According to energy research firm Rystad Energy, about 15 million barrels of crude oil roughly 20 percent of global supply normally pass through the strait daily.

However, threats of missile and drone attacks linked to the conflict have significantly reduced tanker movement through the waterway. The strait serves as a major export route for oil and gas from countries including Saudi Arabia, Kuwait, Iraq, Qatar, Bahrain and the United Arab Emirates.

Meanwhile, Iraq, Kuwait and the UAE have reportedly reduced oil production as storage facilities become filled due to limited export capacity.

Attacks on Energy Facilities

Since the conflict began on March 1, strikes targeting oil and gas infrastructure have intensified concerns about global supply shortages. Authorities in Iran reported that Israeli strikes on oil depots in Tehran and a petroleum transfer terminal killed four people.

Israeli officials claimed the facilities were being used by Iran’s military to supply fuel for missile launches.

Iran currently exports about 1.6 million barrels of oil per day, with most shipments going to China. Any disruption to these exports could further tighten global supply and drive prices higher.

Impact on Consumers and Markets

Rising oil prices have already begun affecting consumers and financial markets.

According to the AAA (American Automobile Association), the average price of regular gasoline in the United States climbed to $3.45 per gallon, about 47 cents higher than a week ago. Diesel prices rose to around $4.60 per gallon, an increase of about 83 cents within the same period.

Speaking on State of the Union (CNN program), U.S. Energy Secretary Chris Wright said gasoline prices could fall below $3 per gallon again in the near future.

“Even in the worst case, this situation is likely to last weeks rather than months,” he said.

Financial Market Reactions

The spike in energy prices has unsettled global financial markets, raising fears that higher fuel costs could trigger inflation and slow consumer spending.

Futures tied to the S&P 500 dropped 1.6 percent, while the Dow Jones Industrial Average futures fell 1.8 percent. Futures linked to the Nasdaq Composite declined 1.5 percent, signaling potential losses when markets reopen.

Analysts warn that if oil prices remain above $100 per barrel for a prolonged period, the strain on the global economy could intensify.

Natural gas prices have also risen during the conflict, though at a slower pace, reaching $3.33 per 1,000 cubic feet, about 4.6 percent higher than the previous closing price.